For all these Europhile progressives who’ve held out that reform is the best way to take care of the neoliberalism of the European Union and even, in some instances, claimed that the austerity mindset was over (as soon as the fiscal guidelines enshrined within the Stability and Progress Pact had been quickly suspended throughout the pandemic), the behaviour of the French authorities ought to wake them out of their delusional reverie. The brand new Prime Minister addressed the Nationwide Meeting final week and outlined a brand new fiscal route involving important expenditure cuts and tax hikes. His plan is not going to fulfill the European Fee, nonetheless, who below the Extreme Deficit Protocol (EDP) have indicated they need a quicker transition again to the fiscal rule thresholds (that’s, even harsher austerity than Barnier is proposing). This coverage shift is within the context of an elevated unemployment fee (which is rising) and an already important output hole. The austerity is more likely to push the unemployment fee in direction of 9 per cent (round) and shall be a catastrophe for the prosperity of the French people who find themselves nonetheless enduring the cost-of-living fallout from the pandemic and the Russian-Ukraine scenario. Add within the potential impacts of the Center East disaster and we have now a failed state. As soon as once more the fiscal guidelines outlined throughout the EMU structure are going to ship stunning outcomes.

I final wrote about this subject on this weblog submit – The 20 EMU Member States will not be foreign money issuers within the MMT sense (September 16, 2024) – in response to some commentators with MMT leanings claiming that the unique structure of the Financial and Financial Union has been ‘modified’ in such a approach that the unique constraints on Member States now not apply.

I argued that whereas the ECB continues to run its bond-buying applications, which successfully controls yield spreads for the 19 Member States of the Eurozone (Germany is the twentieth and the benchmark asset upon which the spreads are expressed), the actual fact stays that the ECB calls for conditionality.

Conditionality within the EU context means austerity.

The European Fee authorities have now ended the ‘normal escape clause’ of the Stability and Progress Pact and are as soon as once more implementing the Extreme Deficit process (EDP) and imposing austerity on a number of Member States.

The non permanent rest of the SGP guidelines (through the overall emergency clause) didn’t quantity to a ‘change’ within the fiscal guidelines.

Certainly, the EDP has been strengthened this yr.

The Member States nonetheless face credit score danger on their debt, nonetheless use a overseas foreign money that’s issued by the ECB and is past their legislative remit, and are nonetheless susceptible to austerity impositions from the Fee and their technocrats.

And now we’re seeing the austerity dialogue translating into precise coverage shifts in France.

Final week (October 1, 2024), the brand new French Prime Minister Michel Barnier, who was foisted into the position by the President’s defiant disregard for the outcomes of the latest election, gave his first speech to the French Nationwide Meeting.

The speech got here at merchandise 4 on the agenda – 4. Déclaration du Gouvernement et débat.

After some recognition for the stunning homicide of the feminine pupil often called ‘Philippine’ in Bois de Boulogne just a few weeks in the past, Barnier turned to his temporary.

He mentioned to the astonishment of many Meeting members:

Contrairement aux termes de l’ordre de mission signé par le général de Gaulle, nous ne partons pas de « presque rien ». (Exclamations et applaudissements sur de nombreux bancs du groupe EPR.) Je pars, avec le Gouvernement, d’un vote populaire par lequel vous avez été élus, mesdames, messieurs les députés …

Paraphrasing – he claimed that the federal government was elected by fashionable vote – joke.

The transcript recorded “Rires et exclamations sur les bancs des groupes LFI-NFP, EcoS et GDR)” (laughter and exclamations from the benches of the LFI-NFP, EcoS and GDR).

The progressive members will deliver a vote of no confidence in Barnier within the coming interval.

He then turned to presenting “le Gouvernement notre feuille de route” (the federal government’s highway map) which comprised “cinq grands chantiers” (5 main initiatives).

I’ll simply present my translated model from right here to avoid wasting area.

The primary of those main initiatives – predictably – was chopping public debt – he mentioned there was a “sword of Damocles hanging over the Authorities” (to which somebody cried out “It’s Macron”).

He mentioned:

The actual sword of Damocles is our colossal monetary debt: €3,228 billion. If we aren’t cautious, it’ll place our nation getting ready to a precipice. This yr, our public deficit, that of all public authorities, is predicted to exceed 6% of GDP.

He invoked the grandchildren fable and mentioned that “the burden of this debt – 51 billion euros – is the second largest merchandise of presidency expenditure, behind training.”

He mentioned they needed to cut back debt to “regain the budgetary room to maneuver”.

He promised to scale back the deficit in 2025 to five per cent of GDP and attain the three per cent threshold below the SGP by 2029.

It’s moot whether or not the European Fee will settle for that delay given they’ve demanded below the EDP that France obtain the three per cent threshold by 2027.

The projections this yr are for the fiscal deficit to transcend 6 per cent of GDP, regardless of the final authorities below former Finance Minister Bruno Le Maire promising it will be a 4.4 per cent, which quickly placated the Fee technocrats.

The projected debt ratio is now 112 per cent of GDP and France pays extra curiosity on its excellent debt than Spain or Greece, which is not any shock given how austerity has ravaged these nations.

He mentioned the one approach they might try this was to “cut back spending” such that “two-thirds of the shift again to five per cent would are available in that approach”.

He’s additionally dedicated to “searching down duplication, inefficiencies, fraud, abuse of the system and unjustified rents” throughout the public sector.

AKA Austerity.

He additionally mentioned that elevated taxes would comprise the remaining third of the fiscal adjustment.

These would principally come from extremely worthwhile firms and rich French taxpayers.

The opposite main initiatives associated to addressing local weather change, immigration (extra prisons and police to maintain the immigrants at bay), and safety, partially, to appease the opposite members who ought to have been allowed to kind the federal government if Macron had revered the voting outcomes.

But it surely was the declare that France has a “colossal fiscal deficit” that dominated his speech.

In case you are questioning why the fiscal scenario has arisen then it is not going to shock you that the French authorities took what they known as their “no matter it takes” strategy to the latest crises – pandemic, yellow vests, and the inflation spike from the Russian scenario.

The fiscal outlays in pursuing this strategy had been bigger than the spending of different Eurozone nations.

On this article from the French analysis physique – Observatoire français des conjonctures économiques – (Could 24, 2024) – Les crises expliquent-elles la hausse de la dette publique en France? – we find out how the rise in public debt has occurred.

Their graph exhibiting debt as a p.c of GDP exhibits the affect of coping with successive crises.

They conclude that:

1. Between 2016 and 2023, 52 per cent of the rise in public debt was not linked to everlasting fiscal settings.

2. So whereas the debt ratio rose by 12.2 per cent of GDP over this era, 6.6 factors of that had been as a result of crises.

3. Nonetheless, they estimate that this proportion rises to 69 per cent if the “l’esnsemble du plan de relance” (total restoration plan) is taken into account (that’s, together with the response to the Yellow Vests – the cheaper petrol subsidies and so forth).

4. Between 2007 and 2023, the response to the crises elevated public debt by 44 per cent.

These had been reliable makes use of of fiscal coverage to avoid wasting the nation from disaster but they find yourself violating the fiscal guidelines of the EMU and now require harsh cuts below the EDP.

What’s the context that the French authorities is now being compelled to make these cuts?

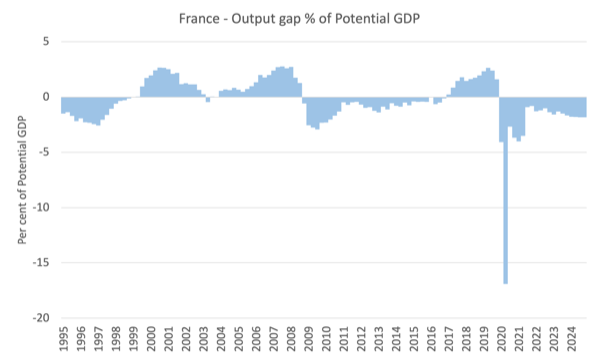

The following graph exhibits the output hole (from the OECD) as a per cent of potential GDP.

I contemplate the OECD collection to understate the scale of the output hole by some factors (and definitely their methodology biases the result in favour of a zero output hole which constitutes full employment).

However even with these biases, the present output hole is critical.

I also needs to add that the potential GDP collection exhibits a major flattening because the GFC, which implies that the French financial system has much less capability to provide GDP progress and meaning there was a deterioration within the relationship between labour drive aggregates and the nationwide accounts aggregates.

It implies that a slower precise GDP progress will produce smaller output gaps but be related to a bigger downside.

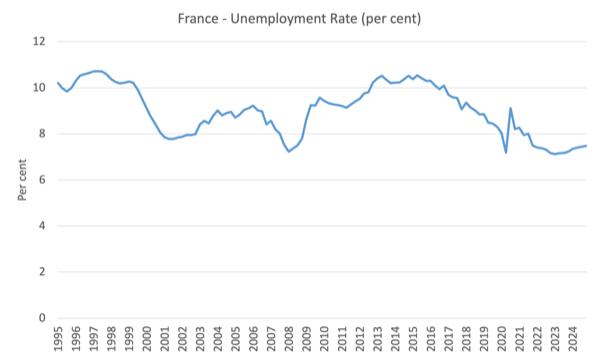

The following graph exhibits the evolution of the unemployment fee since 1995.

It’s at the moment at 7.4 per cent and rising.

These aggregates will deteriorate additional with this renewed austerity push by the Authorities below stress from the European Fee.

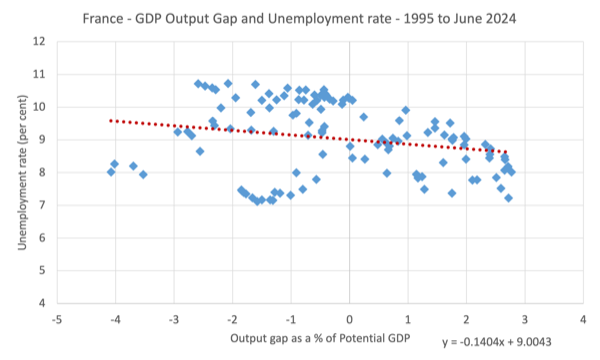

The following graph exhibits the connection between the output hole (horizontal axis) and the unemployment fee (vertical axis).

I disregarded the commentary for the June-quarter 2020 when the output hole was estimated to be 16.92 per cent – it will have skewed the graph.

The purple dotted line exhibits a easy linear regression linking the 2 aggregates (and the equation proven defines that dotted line).

This desk exhibits the estimated unemployment fee for various assumptions in regards to the output hole (utilizing the equation generated within the final graph).

| Output Hole (%) | Unemployment Charge (%) |

| -2.00 | 9.29 |

| -2.25 | 9.32 |

| -2.50 | 9.36 |

| -2.75 | 9.39 |

| -3.00 | 9.43 |

The present output hole is -1.86 per cent.

So even when the output hole will increase by lower than 1 level, the unemployment fee will rise to over 9 per cent as an approximation.

Conclusion

The issue going through the French authorities is that the austerity they’re planning to inflict on the nation is incompatible with the opposite challenges that Barnier outlined in his speech, particularly coping with decarbonisation and local weather points.

However furthermore, the French case demonstrates the dysfunctional nature of the fiscal guidelines that outline the structure of the frequent foreign money.

A authorities is caught in a bind – it has to bail the financial system out throughout crises, however in doing so it realises that it should pay the piper with harsh austerity as a consequence.

The Eurozone is trapped on this perpetual cycle of 1 step ahead, a number of steps again on a regular basis purely because of the foundations that aren’t match for objective.

Nothing a lot has modified within the final 24 odd years of operation.

And the progressives who suppose there may be reform hope are sorry to say hopelessly mistaken.

Sure, the ECB continues to be shopping for the debt and protecting Member State governments above water.

However the conditionality and the remainder of the fiscal guidelines structure nonetheless exerts affect and undermines prosperity.

What a depressing place Europe has turn out to be below the present political class.

Finally, it’s hoped, the residents stand up and abandon this depressing system.

At the least the French have achieved that previously.

That’s sufficient for immediately!

(c) Copyright 2024 William Mitchell. All Rights Reserved.