SOL

en

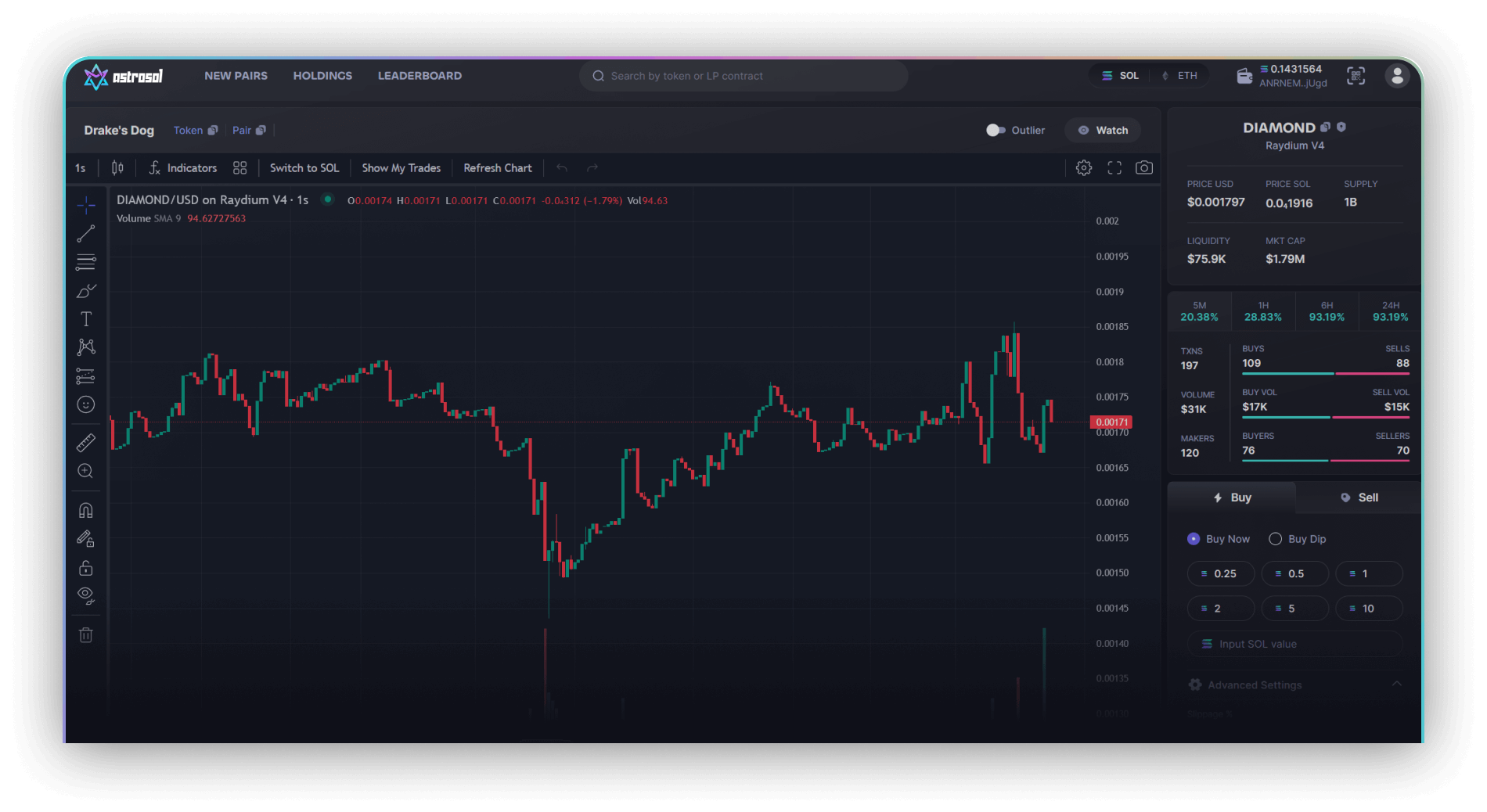

Snipe and sell

tokens

at

at

lightning speed

Connect to start trading

SOL

now

Connect wallet

By connecting, I agree to the

Terms

&

Privacy

GAINS WITH ASTROSOL

BHQ...GKG sold $WYNN for

+2,837%

HXf...jmx sold $HOPPY for

+1,578%

FEC...yAS sold $BONG for

+1,240%

Built by traders

for traders

01.

Discover

Discover new tokens and filter by your preferences.

Connect

02.

Monitor

Real-time security updates & easily monitor your portfolio.

Connect

03.

Quick Buy and Sell

Trade faster with AstroSol with a speed advantage for every transaction.

Connect